The High-Stakes Race for Generic Market Entry

Imagine a race where the winner gets to charge almost the same price as the original brand-name drug for six months. That is the reality of the generic drug market. But what happens when the first runner crosses the finish line? The game changes instantly. This article breaks down how subsequent competitors enter the market after the first generic approval, why prices crash so hard, and the strategic moves companies make to survive.

We are looking at a system governed by the Hatch-Waxman Act of 1984, which created a sequential entry model. It’s not just about who gets FDA approval first; it’s about who can navigate litigation, manufacturing, and distribution hurdles fastest. If you are trying to understand why your medication cost dropped from $300 to $10 in a year, or why some drugs stay expensive despite "generics" being available, the answer lies in this complex dance of multiple entrants.

The 180-Day Exclusivity Window

The first generic competitor to successfully challenge a brand drug's patent receives a massive advantage: 180 days of marketing exclusivity. During this window, they are the only generic allowed on the market. This isn't just a formality; it’s a financial lifeline. Challenging patents costs between $5 million and $10 million in legal fees. The exclusivity period allows the first entrant to recoup these costs by capturing 70-80% of the market share at prices ranging from 70-90% of the brand name price.

This phase is critical. According to data from the Federal Register, the clock starts ticking only when the drug is first marketed or when a court rules the patent invalid. Until then, the brand name company holds all the power. Once that first generic hits pharmacy shelves, the exclusivity timer begins. For the next six months, the first generic enjoys premium pricing. However, this period is under constant threat from the brand name company itself, which often launches an "authorized generic" to disrupt the newcomer's monopoly.

Authorized Generics: The Brand’s Counterattack

You might wonder why a brand name company would sell its own generic version. It’s a defensive strategy. An authorized generic (AG) is produced by the brand name manufacturer but sold under a different label. Between 2010 and 2019, there were 854 authorized generic launches in the US. About three-fourths of these launched *after* traditional generic competition began, and roughly 70% entered during the first generic’s 180-day exclusivity period.

Why do this? To protect revenue. When a brand launches an AG during the exclusivity window, the first generic’s market share plummets from the typical 70-80% down to 40-50%. Their revenue drops by 30-40%. Take Januvia (sitagliptin) as an example. In December 2019, Merck launched an authorized generic through a subsidiary on the exact day the first generic entered. Within six months, the AG captured 32% of the market share. This move keeps money within the brand company’s ecosystem while technically complying with generic competition laws. For subsequent independent generic entrants, this means the playing field is already tilted before they even arrive.

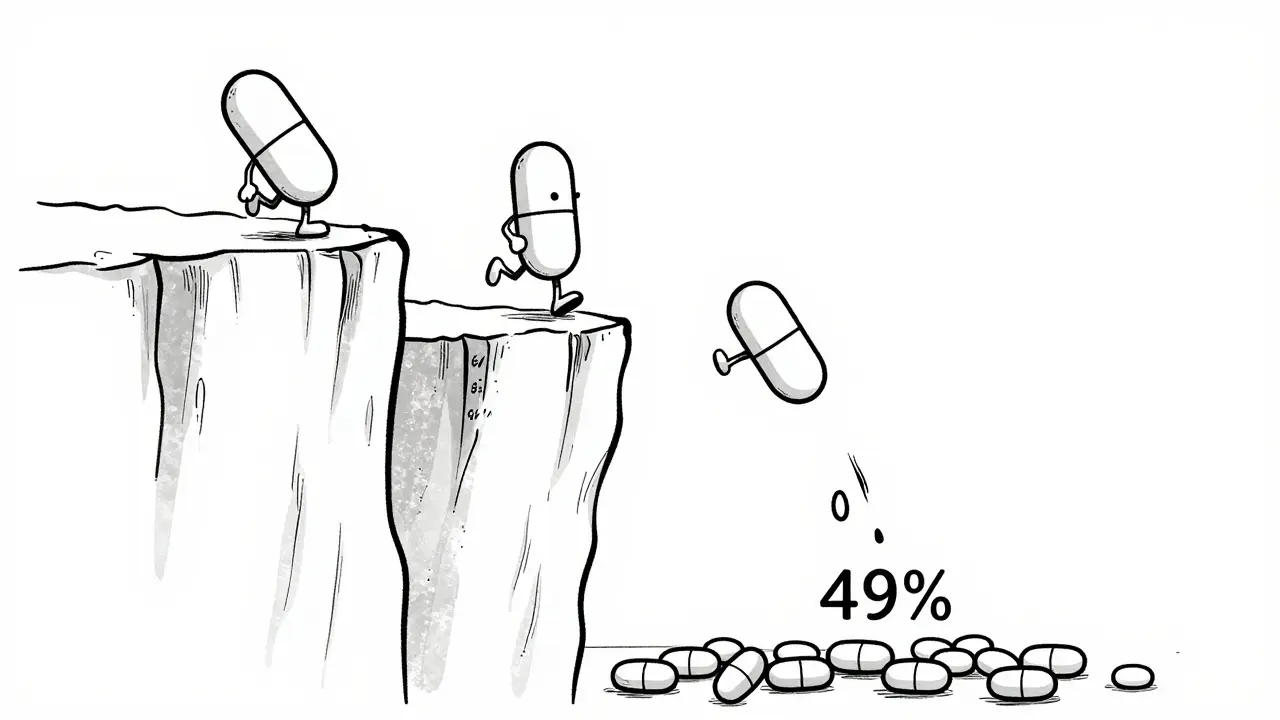

The Price Cliff: What Happens When More Competitors Arrive?

Once the 180-day exclusivity expires, the floodgates open. This is Phase 2 of the market lifecycle, and it is characterized by dramatic price erosion. The FDA’s 2022 report on generic competition shows a clear pattern:

- One generic competitor: Prices average 83% of the brand price.

- Two competitors: Prices drop to 66%.

- Three competitors: Prices fall to 49%.

- Four competitors: Prices hit 38%.

- Five or more competitors: Prices stabilize at approximately 17% of the original brand price.

The steepest decline-often 25-30%-occurs between the second and third entrants. Consider Crestor (rosuvastatin). In 2016, the brand price was $320 per month. Within 18 months of multiple generic entry, eight manufacturers were competing, and the price fell to $10 per month. This rapid erosion creates a "winner-take-all" environment. Subsequent entrants must be ready to compete on razor-thin margins. They cannot rely on premium pricing; they must rely on volume and efficiency.

Strategic Timing and Regulatory Hurdles

Entering after the first generic requires precise timing. Companies watch patent litigation outcomes, manufacturing capacity, and competitor actions closely. While the first generic bears the brunt of patent challenges, subsequent entrants can rely on that work, reducing their development costs by 30-40%. However, they still face regulatory hurdles. The FDA may require additional bioequivalence testing for complex generics, adding 6-12 months to time-to-market.

A major shift occurred with the CREATES Act of 2020. Before this law, brand companies could delay providing necessary drug samples for testing, taking an average of 18.7 months. Now, the average acquisition time has dropped to 4.3 months. This accelerates subsequent entry significantly. On the flip side, brand companies have found new ways to delay competition. The FTC reported that between 2018 and 2022, brands filed 1,247 citizen petitions targeting products with one generic already approved. Each petition typically delays subsequent generic entry by 8.3 months. It’s a cat-and-mouse game of legal maneuvering.

Distribution Wars: Winning the PBM Contracts

Getting FDA approval is only half the battle. The real fight happens in distribution. In 2022, 68% of generic drug contracts used "winner-take-all" models. These contracts award 100% formulary placement to a single manufacturer. This creates a "second first-mover advantage." The first generic to secure Pharmacy Benefit Manager (PBM) contracts captures 80-90% of the market share, regardless of who got FDA approval first.

Subsequent entrants face steep barriers here. They must negotiate with Group Purchasing Organizations (GPOs) that demand 30-40% price concessions, compared to 20-25% for the first generic. It takes an average of 9-12 months for later entrants to achieve formulary placement with major PBMs. During this lag, they capture only 5-10% of the market share. This dynamic forces many smaller generic companies to exit the market or consolidate. The number of active ANDA holders dropped from 142 in 2018 to 97 in 2022, according to the Generic Pharmaceutical Association.

Shortages and Market Instability

The aggressive price competition leads to instability. When prices drop too low, manufacturers struggle to maintain profitability. This often results in production cuts or quality issues. The FDA’s 2022 shortage report noted that 62% of generic drug shortages involved products with three or more manufacturers. Many of these shortages stem from shared contract manufacturing organizations (CMOs). Second-and-later entrants increasingly rely on CMOs (78% vs. 45% for first entrants) to reduce capital investment. If one CMO has a quality issue, it affects multiple brands simultaneously.

In 2022, 37% of generic drug markets experienced shortages within 18 months of multiple generic entry. Compare this to only 8% during the first generic’s exclusivity period. The volatility makes it difficult for supply chains to remain stable. Experts like Dr. Aaron Kesselheim argue that the current system creates perverse incentives where too many companies enter simple generic markets too quickly, leading to unsustainable price competition. Former FDA Commissioner Dr. Scott Gottlieb has advocated for market-based solutions like restricted entry or long-term contracting to stabilize the market.

Biosimilars: A Different Game

It is important to distinguish small-molecule generics from biosimilars. Biosimilars are biological products similar to an already approved biological medicine. They are more complex to manufacture and develop, costing $100-250 million per product. Consequently, the price erosion is slower. With two biosimilar competitors, prices average 70-75% of the reference product. With four or more, they drop to 50-55%. Unlike simple generics, biosimilar markets rarely see the extreme saturation of five-plus competitors driving prices to 10-15% of brand levels. By 2027, analysts predict that 70% of simple generic markets will have five or more competitors, while complex generics and biosimilars will maintain 2-3 competitors with higher price points.

| Number of Competitors | Average Price (% of Brand) | Market Dynamics |

|---|---|---|

| 1 Generic | 83% | Exclusivity period; high margin |

| 2 Generics | 66% | Initial competition; AG threats |

| 3 Generics | 49% | Steepest price drop (-25-30%) |

| 4 Generics | 38% | Volume-driven sales |

| 5+ Generics | 17% | Saturation; winner-take-all PBMs |

Future Outlook: Efficiency vs. Innovation

The industry is splitting into two categories. "Innovation players" focus on complex generics with limited competition, avoiding the price wars of simple drugs. "Efficiency players" compete on cost in saturated markets, relying on scale and lean operations. With the OECD noting that the US experiences the most rapid price erosion globally (reaching 10-15% of brand levels within 24 months), only the most efficient manufacturers will survive. For patients, this means lower prices but potential access issues due to shortages. For investors and policymakers, it highlights the need for reforms that balance competition with supply chain resilience.

What is the 180-day exclusivity period?

The 180-day exclusivity period is a regulatory incentive under the Hatch-Waxman Act. It grants the first generic competitor to challenge a brand drug's patent exclusive marketing rights for 180 days. This allows them to recover litigation costs and earn higher profits before other generics can enter the market.

Why do prices drop so sharply after the third generic enters?

The entry of a third generic triggers intense competition. Data shows prices fall from 66% of brand value with two competitors to 49% with three. This is because the market shifts from duopoly dynamics to oligopoly, forcing manufacturers to cut prices drastically to win Pharmacy Benefit Manager (PBM) contracts and market share.

What is an authorized generic?

An authorized generic is a drug produced by the brand name manufacturer but sold under a different label, often at a lower price. Brands launch these to protect their revenue streams during the first generic's exclusivity period, effectively competing against themselves to limit the first generic's market share.

How do PBMs affect generic drug availability?

Pharmacy Benefit Managers (PBMs) use "winner-take-all" contracts, giving 100% formulary placement to one manufacturer. This creates a bottleneck where only one or two generics dominate sales, making it hard for subsequent entrants to gain traction and contributing to market consolidation and occasional shortages.

Are biosimilars cheaper than traditional generics?

No, biosimilars generally remain more expensive. Due to higher development costs ($100-250 million) and complex manufacturing, biosimilar prices stabilize at 50-55% of the reference product price even with four or more competitors, whereas simple generics can drop to 17%.

What role does the CREATES Act play in generic entry?

The CREATES Act requires brand companies to provide drug samples needed for generic testing. This reduced the average sample acquisition time from 18.7 months to 4.3 months, significantly accelerating the entry of subsequent generic competitors into the market.

Why are there frequent shortages in multi-generic markets?

Low prices in saturated markets squeeze profit margins, leading manufacturers to cut corners or exit production. Additionally, reliance on shared contract manufacturing organizations (CMOs) means a quality issue at one facility can cause shortages across multiple brands, accounting for 62% of generic shortages in products with three or more manufacturers.

How long does it take for a new generic to get formulary placement?

It takes subsequent generic entrants an average of 9-12 months to achieve formulary placement with major PBMs. During this period, they capture only 5-10% of the market share, facing significant headwinds from established competitors who hold exclusive contracts.